Client Login

Client Login

How to protect your retirement from inflation

It’s the ultimate battle of good vs evil. Retirement vs. Inflation. Inflation is the arch-enemy of your retirement savings and if you’re near retirement – or even thinking about it – now is a good time to pay particularly close attention to your money. According to the Bureau of Labor Statistics Press Release on January 12, 2022, it is clear that prices are rising and inflation is here. Overall, prices have climbed 7% year over year which is the greatest increase in over 40 years. Truly there is no other topic that seems to be getting more attention right now than inflation.

On top of that, the pandemic has most certainly shaken the sense of security that Americans felt when it comes to their finances and a lot of people feel more vulnerable than they did two or three years ago. Even if you have been diligent about saving for retirement inflation can eat into your nest egg quickly.

Why Inflation Happens

Inflation is, oddly, both incredibly simple to understand and absurdly complicated. It is worth taking a pause and understanding why inflation is happening in the first place.

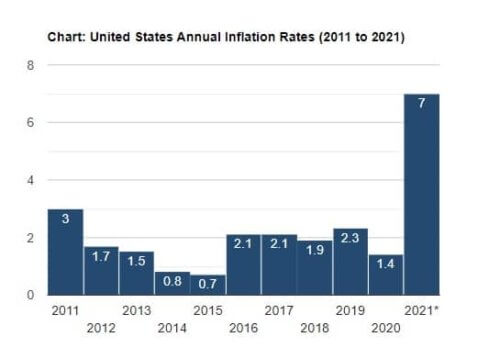

In the simplest terms, inflation happens when prices broadly go up. In other words, the average price of everything is increasing (housing, food, gas, cars, etc.). Generally, it is not a bad thing, as wages also rise. Ideal inflation according to the U.S. Federal Reserve targets an annual inflation rate of 2%. Most policymakers believe it leads to a healthy economy. However, we are currently sitting at 7%. A bit off the mark is an understatement. Here is a visual to give you an idea of where we are in relation to just 10 years ago.

Source: US Inflation Calculator

Why is inflation so high right now?

Again, simply put…blame the pandemic. In response to the pandemic, the Fed started adding an unprecedented amount of money into the economy via emergency stimulus funds to quickly get the country out of the recession, plus they slashed interest rates. People started spending more and demand was up. Good, right?

Yet, months and months of this fueled inflation because supply wasn’t able to recover as fast. Take for example the automobile industry. Many auto-manufacturers shut down during the pandemic and were slow to get things moving again, some still are, mostly due to supply chain issues. It is a classic formula of high demand plus limited supply equals higher prices.

Further, inflation is hard to predict because it depends on what people expect of inflation in the future. For example, if businesses expect higher prices and wages next year, they’ll raise prices now. If workers expect higher prices and wages next year, they’ll ask for higher wages now. So Fed Chairman Jerome Powell has long been calling the recent inflation “transitory”, meaning in other words, only a temporary correction of the pandemic.

However, both Powell and Treasury Sectary Janet Yellen admitted last month (December 2021) that it is time to retire the term. So, prices will continue to go up and the government is finally admitting it. Now what?

How to protect your retirement from inflation

Maximize Social Security Benefits

With rising costs it may be hard to offset inflation with your traditional retirement benefits, such as social security. However, you can work to maximize your social security benefits by delaying them. Delayed Retirement Credits help you to increase your benefit by a certain percentage each month that you delay starting your benefits. If you can wait to start getting your social security checks until age 70 your monthly payments will be higher and will adjust to the annual cost of living when you do begin to take them.

It is important for everyone to maximize their social security benefits. This is a small step that could potentially hedge off some inflation and help your retirement savings go a little further.

Get aggressive with any Consumer Debt

The Feds have signaled it will aim to make some aggressive policy moves in response to the current situation. It is likely we may see as many as three rate hikes this year, two more next year, and another two in 2024. If you have any outstanding credit card debt now is the time to pay it down before interest rates go up. Any variable rate debt will get very pricey. If you cannot pay it off all at once, but you have good credit try and take advantage of some zero to low-interest balance transfers. Doing this will help insulate you from the coming higher interest rates.

Take advantage of lower mortgage interest rates now

While mortgage rates move based on long-term bond yields, a spike in consumer prices will certainly make a rise in mortgage rates more likely. Right now mortgage rates are still low. If you have considered refinancing to a lower rate (or buying a new home) this is your sign to look into it further depending on the term left on your mortgage. If rates do go up, you may wish you would have done it sooner. Also, as mentioned above, if you have an adjustable home equity line it could be at risk for an increase. Call a mortgage broker today to see what options you have.

Look at your portfolio and make adjustments as needed

As financial advisors, this is something we are watching closely. Here are some of the general recommendations we have, however, everyone’s financial situation is different so we recommend contacting us (or talking to CERTIFIED FINANCIAL PLANNER™) before making any changes. Also, keep in mind if rates don’t go up like crazy these recommendations may not be the best and may underperform your hopes.

First, at the very least, review your investment allocations. If you have bonds in your portfolio, we recommend short-term bond funds until interest rates go up. Ultimately these are going to be less risky with rising interest rates. While they may not have as much earning potential they can weather the inflation storm better.

Also, with rising prices, finding stocks with dividends can add value to a portfolio. Think consumer-based large-cap stocks. Likewise, financial stocks also commonly benefit from higher prices and inflation. These types of investments may help keep pace during an inflationary environment.

Finally, consider diversifying with Digital Assets, such as Bitcoin. Essentially, owning Bitcoin means you are betting against the world’s fiat currencies. Most major digital assets have a fixed number of coins or have capped the potential circulation growth. Interestingly, the infamous billionaire investor, Paul Tudor Jones, has even claimed that crypto protects better against inflation than gold. While there still may be limited evidence that crypto can hedge inflation and will cure all as it itself is often susceptible to market jitters, it certainly is worth looking into if it fits your risk tolerance and time horizons.

Again, we emphasize not making any dramatic changes to your investments until you’ve consulted with a professional. Our experience has taught us that unforeseen events can happen and do happen, so it is best to stay diversified, rebalance as needed, and always come back to your long-term goals. We are happy to talk with you about your specific situation anytime. Schedule a call here.

In conclusion

Inflation can impact your retirement in a variety of ways. If you’re not on the right path to protect yourself against inflation it will be increasingly difficult for you to live comfortably when you can are no longer working. Adjusting your investment strategy, spending habits, and expectations to account for inflation is extremely important for retirees and those close to retirement.