By 2033, Social Security benefits are projected to be reduced by about 25%. That’s not speculation, that’s straight from the Social Security Administration.

And if nothing changes long term, those cuts could get even worse. That matters more than most people realize.

If you’re expecting $2,000 a month, a 25% reduction brings that down to $1,500. That’s $6,000 a year gone. For many retirees, that’s the difference between feeling stable and feeling stressed every single month.

Here’s the part most people miss: Your Social Security benefit is not fixed.

There are real, practical moves you can make right now that can increase what you receive for the rest of your life. Below are five of the most impactful strategies to help you get the most out of what you’ve earned.

Keep reading, or if you prefer to listen or watch… check out the Podcast or full YouTube video.

First, How Social Security Actually Works

Before we get into the strategies, it helps to understand how your benefit is calculated.

Every paycheck you’ve earned included a 6.2% contribution to Social Security (your employer matched it). Over time, that adds up.

When it’s time to calculate your benefit, the government:

Adjusts your earnings for inflation

Takes your 35 highest earning years

Averages them out over 420 months

Runs that number through a formula to determine your monthly benefit

That final number is called your Primary Insurance Amount (PIA), which is what you receive at full retirement age.

Everything you’re about to read either increases or decreases that number.

1. Work at Least 35 Years

This is one of the most overlooked factors.

If you don’t have 35 working years, Social Security doesn’t adjust the formula. It still divides by 420 months, which means missing years show up as zeros.

Those zeros drag your average down, and that lowers your benefit permanently.

The fix doesn’t have to be extreme. Even part-time work or side income in later years can replace a zero with a real number, and that can increase your monthly benefit more than you might expect.

2. Replace Low-Earning Years

Even if you already have 35 years, you’re not done.

Your benefit is based on your highest 35 years. That means lower-earning years still bring your average down.

If you’re earning more now than you did earlier in your career, continuing to work can replace those lower-income years with higher ones.

For example, replacing a $20,000 earning year with a $100,000 year can meaningfully increase your average and your future benefit.

Before stepping back or retiring early, it’s worth understanding what that decision could cost you long term.

3. Delay Filing (If It Makes Sense)

This is one of the most powerful strategies available.

You can start collecting Social Security at age 62, but there’s a trade-off:

You’ll lose about 6% per year you claim early

That reduction is permanent

On the flip side:

For every year you delay past full retirement age (up to 70), your benefit increases by about 8% per year

That can add up quickly.

A benefit of $2,300 at full retirement age could grow to nearly $2,900 by waiting a few years. And since Social Security adjusts for inflation, that higher base compounds over time.

This isn’t a one-size-fits-all decision. Health, income needs, and life expectancy all matter. But if you’re able to delay, it’s often one of the most effective ways to increase your lifetime benefit.

4. Coordinate Spousal Benefits

If you’re married, this is where strategy really matters.

Social Security isn’t just an individual decision; it’s a joint one.

A lower-earning spouse can receive up to 50% of the higher earner’s benefit, but timing is critical. Claiming early reduces that amount.

There’s also an important long-term consideration:

When one spouse passes away, the surviving spouse keeps the higher of the two benefits.

That means the higher earner’s decision about when to file doesn’t just affect them, it can directly impact their spouse’s financial security for the rest of their life.

Coordinating your strategy as a couple can make a significant difference.

5. Check Your Earnings Record

This might be the most underrated strategy on the list.

The Social Security Administration has acknowledged that billions of dollars in wages have gone unmatched to the correct records.

If your earnings history is wrong, your benefit could be lower than it should be, and you may never know unless you check.

Here’s what to do:

Create an account at SSA.gov

Review your earnings history year by year

Compare with old W-2s or tax returns if something looks off

Fixing an error could increase your monthly benefit for the rest of your life, and it might only take 30 minutes to catch.

Why This Matters More Than Ever

Over 40% of retirees rely on Social Security as their primary source of income. Even for those with savings, it often forms the foundation of a retirement plan. Small decisions made today can have a six-figure impact over time.

The five strategies are simple:

Work 35 years if possible

Replace lower-earning years

Delay filing when it makes sense

Coordinate with your spouse

Check your earnings record

None of these are complicated, but they do require awareness and intentional planning.

The Bottom Line

You’ve been paying into Social Security your entire working life.

It’s worth taking the time to understand how it works and making sure you’re getting everything you’ve earned.

Most people spend more time planning a vacation than they do planning this.

That’s a mistake you can avoid.

Next Steps.

If you want to look at your specific situation and figure out the right Social Security strategy for you, that’s exactly what we do. At Bonfire Financial, we help you coordinate your taxes, investments, and income into one clear plan so you can move forward with confidence.

Before you make any decisions, grab our free Social Security Cheat Sheet with the updated 2026 numbers. It’s a quick, easy reference that breaks down when to claim, how benefits are calculated, and the key thresholds you need to know. Download it and make sure you’re not leaving money on the table.

When it comes to your Medicare choice, the decisions you make at age 65 (or even slightly before) can have long-lasting consequences. Yet many end up choosing a plan based on general advice, slick marketing, or a brief conversation with their benefits department.

To help cut through the confusion, we sat down with Andrew Mersereau, a Medicare specialist with over 24 years of experience guiding individuals through enrollment, plan selection, and strategy. Andrew is known for his no-nonsense, education-first approach to Medicare and has helped countless clients avoid costly mistakes.

Today we’re breaking down everything you need to know to make a confident, well-informed Medicare choice that fits your needs, especially if you’re financially secure, still working at 65, or considering a Roth conversion or property sale that could spike your income.

Before diving into strategies, it’s helpful to revisit the basics. Medicare is a federal health insurance program for people 65 and older, as well as some younger individuals with disabilities. But “Medicare” isn’t one plan, it’s a collection of parts:

Part A: Hospital coverage (inpatient)

Part B: Medical coverage (outpatient care, doctor visits, preventive services)

Part C: Medicare Advantage plans offered by private insurers as an alternative to A and B

Part D: Prescription drug coverage

Original Medicare (Parts A and B) is provided by the federal government. To cover additional costs and services, many people add Part D and either a Supplement (Medigap) policy or an Advantage plan.

The Big Decision: Supplement vs. Advantage

This is the crossroads most people face, and it’s not as straightforward as it seems.

Medicare Advantage (Part C)

Medicare Advantage plans are offered by private insurance companies and typically include Parts A, B, and D bundled together. These plans often tout extra perks like dental, vision, gym memberships, or transportation to doctor visits.

But those extras come with trade-offs. Advantage plans often:

Have narrow provider networks

Require referrals for specialists

Use prior authorizations for many procedures

Limit care to a specific geographic region

These plans are appealing due to their low or zero-dollar premiums, but you may find yourself paying more out of pocket when you actually need care.

Medicare Supplement (Medigap)

Medigap policies work alongside Original Medicare to pay for out-of-pocket costs like coinsurance, copayments, and deductibles. They do not include drug coverage, so you’d add a standalone Part D plan.

Key benefits of Medigap plans:

See any provider in the U.S. who accepts Medicare—no referrals needed

No network restrictions

Predictable costs with limited out-of-pocket expenses

For frequent travelers, snowbirds, or anyone who wants maximum freedom in choosing providers, Medigap is often the better long-term choice.

“People often pick Advantage for the low monthly price, but later regret the restrictions,” Andrew warns. “Your Supplement choice may cost more monthly, but it gives you far greater control.”

Why Your First Medicare Choice Might Be Permanent

Here’s the part most people don’t realize: the choice you make when you first sign up, especially between Supplement and Advantage, can be extremely hard to reverse.

Under federal law, you’re guaranteed acceptance into any Medigap plan only during your initial enrollment period (usually the six months after you enroll in Medicare Part B). After that window closes:

Insurance companies can ask health questions

They can deny you based on preexisting conditions

Approval becomes much more difficult as you age or develop medical issues

Andrew says it plainly:

“In my experience, 80% of people who try to switch from Advantage to Supplement later are denied.”

This is why the decision you make when you first sign up is so critical. Switching may not be an option later.

IRMAA and Income Traps: What Affluent Retirees Need to Know

Medicare premiums aren’t fixed for everyone. If your income is high, you may be subject to the IRMAA (Income-Related Monthly Adjustment Amount). This surcharge applies to Parts B and D and is based on your Modified Adjusted Gross Income (MAGI) from two years prior.

Janet, 64, sells her investment property and earns a $300,000 gain. Two years later, she’s shocked to find her Medicare premiums more than double, she’s now in an IRMAA tier that costs her over $500 more per month.

These are avoidable surprises, but only with proper planning.

Still Working at 65? Don’t Assume You Can Delay Medicare

Many people working past 65 wonder if they can delay Medicare enrollment. The answer: only if you have credible employer coverage.

Your plan must:

Cover 20 or more employees

Be deemed creditable by Medicare

Meet specific drug coverage standards

If it doesn’t, and you delay enrolling, you may face lifetime penalties based on your Medicare choice.

Mersereau’s advice: always confirm with HR in writing that your coverage meets Medicare’s standards, and compare your total healthcare costs before making a decision.

Important: If you’re still contributing to a Health Savings Account (HSA), enrolling in any part of Medicare makes you ineligible to keep contributing.

Even the best Medicare plans don’t cover everything. Here are the biggest gaps that surprise people:

Hearing aids

Routine dental care

Eyeglasses and eye exams

Long-term care (like assisted living)

Home modifications or private-duty nursing

Unlimited rehabilitation or therapy

You may need private insurance, Medicaid, or a long-term care policy to bridge these gaps. Supplement plans won’t help with most of these either, they’re for traditional medical expenses only.

For Snowbirds and Travelers: Choose Wisely

If you live part of the year in Florida and the rest in Colorado, or travel often, your plan choice is especially important.

Advantage plans are often limited to regional networks, so out-of-state care may not be covered. Supplement plans allow access to any Medicare provider in the country, making them ideal for travelers or dual-state living.

Timeline: What to Do at 63, 64, and 65

Turning 65 is a major milestone, not just for birthdays, but for healthcare decisions that can impact your financial future. To help you stay ahead of deadlines and avoid costly missteps, here’s a step-by-step timeline of what to focus on at ages 63, 64, and in the months leading up to your Medicare choice and enrollment.

Age 63:

Begin tracking your income to anticipate IRMAA brackets

Evaluate if Roth conversions, property sales, or business exits are better done now

Schedule a financial planning session to model different Medicare scenarios

Choose either a Supplement and Part D or an Advantage plan

Get proof of credible coverage from your employer if you’re deferring enrollment

Red Flags to Watch For

Too-good-to-be-true Advantage ads “Free this” and “zero-dollar that” often hide tight restrictions and surprise bills.

Advice from friends Everyone’s situation is different. What works for one person could be a disaster for another.

Brokers pushing one plan type A good broker will help you compare, not sell you the highest-commission product.

Skipping Part D because you take no meds This can result in penalties later. It’s often smarter to enroll in the lowest-cost plan anyway.

FAQ: Quick Medicare Questions Answered

Q: Is it ever smart to go with just A and B? A: Rarely. Without a Supplement or Advantage plan, your out-of-pocket costs are unlimited.

Q: Can I change my mind later? A: With drug plans (Part D), yes. With Supplement plans, possibly, but you may be denied.

Q: What if I have a concierge doctor? A: You can keep them, but you’ll still need A and B, plus coverage for hospitals, specialists, and serious illnesses.

Q: Does my state affect my ability to switch plans? A: Yes. Some states have more lenient rules, but most follow the six-month initial enrollment protection rule.

Final Thoughts: The Smartest Move is an Educated One

Andrew Mersereau emphasizes that education, not advertising, should guide your Medicare choice.

“Don’t just follow an ad or assume what worked for a friend will work for you. Take the time to understand what you’re buying and why.”

And remember, using a Medicare broker doesn’t cost you extra. Rates are set by law, and a good broker can help you avoid expensive mistakes.

Whether you’re helping a parent, preparing for your own retirement, or simply curious about your options, the takeaway is clear: Medicare isn’t something to wing. It’s a decision that affects your access to care, your costs, and your peace of mind for years to come.

Need help navigating Medicare?

You can contact Andrew’s team at 719-955-4991. They offer education-driven guidance with no pressure.

When we think about Social Security, we often associate it with those who need financial help in retirement. But what if you’re financially independent? What if you’ve done everything right, built significant wealth, and no longer rely on a paycheck? Should Social Security still be part of your retirement plan?

The short answer: yes.

Even if you’re wealthy, Social Security benefits still matter, and today we’ll explore why you shouldn’t overlook them, how to think about them strategically, and most importantly, how to maximize your Social Security benefits to fit into your broader financial picture.

Every so often, I speak with individuals who’ve done exceptionally well for themselves. They’re financially independent, own multiple assets, and feel like they’ve already “won the game” when it comes to money. Naturally, they assume Social Security is irrelevant to their situation.

Their mindset tends to be: “Why should I care? I don’t need it.”

And honestly, I get it. If you’ve saved well, built a solid investment portfolio, and have multiple income streams, Social Security may seem like small potatoes. But there are several reasons this thinking may be short-sighted.

Reason #1: You Paid Into It, It’s Your Money

One of the most important things to remember is this: Social Security isn’t a handout.

You paid into the system for decades. Every paycheck you earned, every tax year you contributed, those funds weren’t just donations. You earned credits (40 of them, to be exact) that now qualify you for a benefit. Claiming Social Security is not about need, it’s about reclaiming what’s yours.

Even if the monthly check doesn’t make a big impact on your budget, ignoring your benefit is like leaving money on the table. Think about it: would you willingly skip collecting on a pension or a rental check just because your portfolio is doing well?

Reason #2: It Can Be Strategically Used (Or Reallocated)

Another common argument is: “Even if I take it, I don’t need the income.”

But that’s where a mindset shift is helpful. You don’t have to use the benefit to fund your lifestyle. You can redirect it toward:

The point is: just because you don’t need the income doesn’t mean it shouldn’t be put to good use.

Reason #3: It’s One of the Few Sources of Guaranteed Income

In a world of market volatility and rising costs, guaranteed income is incredibly valuable. Social Security is one of the only income streams that’s inflation-adjusted and backed by the U.S. government.

For wealthy retirees, having another layer of stable income allows more flexibility with your investments. Maybe you want to delay tapping into your IRA to let it grow. Maybe you want to cover basic expenses with guaranteed funds and let your risk assets ride. Social Security gives you options, and options are power.

But Isn’t the System Running Out of Money?

This is a concern many people have, and it’s valid to a degree. We’ve all heard the headlines: “Social Security will be insolvent by 2030.” But let’s look at the facts:

The trust fund reserves are expected to run low by the early 2030s.

This doesn’t mean benefits go away. It means incoming payroll taxes will only cover around 75–80% of scheduled benefits unless action is taken.

Congress has a long track record of addressing funding issues when needed. It’s politically unpopular to cut Social Security benefits for current retirees, and it’s unlikely to happen without major pushback.

So while the system may see adjustments, perhaps higher income thresholds, delayed full retirement ages, or increased taxes, it’s not disappearing.

And in the meantime, your benefit is still valid and accessible.

How to Maximize Your Social Security Benefits

Now that we’ve established why Social Security matters, let’s talk about how to maximize your Social Security benefits. There are a few key levers you can pull:

1. Delay Claiming (If Possible)

Your benefit increases the longer you wait to claim it. Here’s the breakdown:

Full Retirement Age (FRA): For most people, this is between 66 and 67.

Claiming Early (age 62): Results in a permanent reduction of up to 30%.

Delaying Until 70: Increases your benefit by roughly 8% per year past FRA.

If you’re in good health and don’t need the income, delaying until age 70 can provide the largest monthly benefit, up to 76% more than claiming at age 62.

For someone with wealth and longevity, this can be a smart play.

2. Coordinate Spousal Benefits

If you’re married, you may be eligible for spousal or survivor benefits, which can be up to 50% of your spouse’s benefit (or even 100% if they pass away).

This can be especially valuable if one spouse didn’t earn as much or took time out of the workforce. Strategizing when each spouse claims can help you maximize the total household payout over your lifetime.

3. Watch Your Taxes

Social Security benefits can be taxed, especially if you have other sources of income like pensions, dividends, or required minimum distributions (RMDs). Wealthy retirees should work with a Certified Financial Planner to structure withdrawals in a tax-efficient way. With smart planning, you can minimize how much of your Social Security gets taxed and keep more of your benefits.

4. Use Social Security as a Safety Net

Some people worry about the “what-ifs” in retirement. Market crashes. Health issues. Family emergencies.

Even if you’re wealthy now, having Social Security as a consistent income stream adds stability. You may not use it for years, but if something changes—your expenses increase, your portfolio dips, your family situation shifts, you’ll be glad to have it.

Think of it as a built-in buffer in your financial life.

5. Incorporate It Into Your Philanthropy or Legacy Plan

If you don’t need the money and don’t want to keep it, that’s fine. But take it anyway—and repurpose it.

Ideas include:

Direct donations to charity

Annual gifts to heirs

Contributions to 529 plans

Support for causes or communities you care about

The bottom line: you still control how it’s used.

What About the Ethics of Taking It If You Don’t Need It?

Some people hesitate to claim Social Security out of principle. They feel it should “go to someone who needs it more.”

That’s admirable, but not how the system works.

Social Security is not a needs-based program. It’s an earned benefit. If you’re eligible, you have every right to claim it.

If you want to use it for good, do that, but don’t decline it outright. Claim it, then donate it. Help your family. Fund change in the world. It’s still your money.

Final Thoughts: Don’t Leave Money on the Table

Social Security may not be flashy. It may not feel urgent when your net worth is high. But that doesn’t make it irrelevant.

In fact, maximizing your Social Security benefits is a smart move for anyone, regardless of wealth. Whether you reinvest it, give it away, or use it to supplement your lifestyle, it’s a piece of your financial puzzle that shouldn’t be ignored.

You’ve earned it. Don’t leave it behind.

Next Steps

At Bonfire Financial, we help clients of all income levels make informed, strategic decisions about when and how to claim Social Security. We also offer a FREE Social Security and Medicare Guide & Cheat Sheet that’s updated annually to help you assess your options.

Are you turning 65 soon? Turning 65 is a major milestone and pivotal age for your retirement planning. Not only is this an important age for government programs like Medicare and Social Security, but it’s also a perfect time to check other parts of your financial plan, particularly if you’re about to retire. Here are 6 important things to do as you get closer to your 65th birthday to make sure this year and the many years that follow are amazing! (P.S. Read to the end for a special bonus gift for turning 65!!)

What to do when turning 65 and planning for retirement:

Prepare for Medicare

Consider Long Term Care Insurance

Review your Social Security Benefits

Review Retirement Accounts

Update Estate Planning Documents

Get Tax Breaks

“Every day, about 10,000 people in the United States turn 65 — a milestone that triggers important decisions about Medicare, Social Security, and retirement planning.” – Pew Research Center

1. Prepare for Medicare

Medicare is the most common form of health care coverage for older Americans. The program, established in 1965, provides essential health insurance for people age 65 and older, as well as certain younger individuals with disabilities. For many retirees, Medicare replaces employer-sponsored coverage and becomes the foundation of their health care plan. Understanding how and when to enroll, what each part covers (Parts A, B, C, and D), and how it fits with other insurance options is a key part of financial planning as you approach retirement. Making the right decisions can help avoid penalties, reduce out-of-pocket costs, and ensure you’re fully covered.

What is Medicare?

Medicare is basically the federal government’s health insurance program for people 65 or older (or younger with disabilities). Medicare is primarily funded by payroll taxes paid by most employees, employers, and people who are self-employed. Funds are paid through the Hospital Insurance Trust Fund held by the U.S. Treasury.

When can I enroll in Medicare?

Starting 3 months before the month you turn 65, you are eligible to enroll in Medicare, you can also sign up during your birthday month and the three months following your 65th birthday. Essentially, you have a seven-month window to sign up for Medicare. Be mindful of your timing and enrollment because Medicare charges several late-enrollment penalties.

What does Medicare cover?

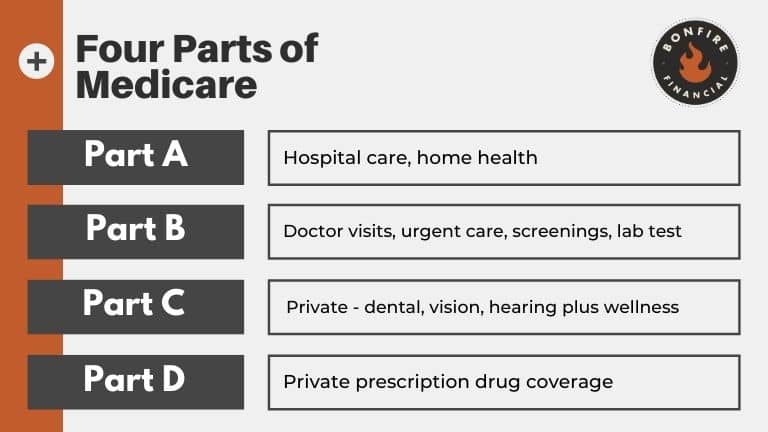

Medicare benefits vary depending on the enrollment plan you choose. Medicare is made up of four enrollment plans: Medicare Part A, Part B, Part C, and Part D.

Here is a quick breakdown of the four parts of Medicare:

Medicare Part A: Know as the Original Medicare, Part A covers inpatient hospital care, home health, nursing, and hospice care. Part A is typically paired with Medicare Part B.

Medicare Part B: Still considered part of the Original Medicare, Part B helps cover doctor’s visits, lab work, diagnostic and preventative care, and mental health. It does not include dental and vision benefits.

Medicare Part C: This option offers traditional Medicare coverage but includes more coverage for routine healthcare that you use every day, routine dental care, vision care, and hearing. Plus, it covers wellness programs and fitness memberships. Medicare Part C is also known as Medicare Advantage and is a form of private insurance. Note that you will not be automatically enrolled in these benefits.

Medicare Part D: Medicare Part D is a stand-alone plan provided through private insurers that covers the costs of prescription drugs. Most people will need Medicare Part D prescription drug coverage. Even if you’re fortunate enough to be in good health now, you may need significant prescription drugs in the future.

While Medicare is great it’s not going to cover all your medical expenses. You’ll still be responsible for co-payments and deductibles just like on your employer’s health plan, and they can add up quickly.

To offset these expenses, a Medicare Supplement (Medigap) insurance policy could be a good option as well. Medigap is offered by private insurance companies and covers such as co-payments, deductibles, and health care if you travel outside the U.S.

How can I enroll in Medicare?

For most people, applying for Medicare is a straightforward process. If you already receive retirement benefits from Social Security or the Railroad Retirement Board, you’ll be signed up automatically for Part A and Part B.

If you aren’t receiving retirement benefits, and you don’t have health coverage through an employer or your spouse’s employer, you will need to apply for Medicare during your 7-month enrollment window.

You can sign up for Medicare online, by phone, or in-person at a Social Security office.

Please note that if you have a Health Savings Account (HSA) or health insurance based on current employment, you may want to ask your HR office or insurance company how signing up for Medicare will affect you.

2. Consider Long Term Care Insurance

Another prudent thing to do when you are turning 65 is to consider your long-term care insurance options before retirement.

What is long-term care insurance?

The goal of long-term care is to help you maintain your daily life as you age. It helps to provide care if you are unable to perform daily activities on your own. It can include care in your home, nursing home, or assisted living facility. The need for long-term care may result from unforeseen illnesses, accidents, and other chronic conditions associated with aging.

Medicare often does not provide long-term care coverage, so it is a good idea to factor this additional coverage in.

Why do I need long-term care insurance?

While it may be hard to imagine needing long-term care now, the U.S. Department of Health and Human Services estimates that someone turning age 65 today has almost a 70% chance of needing some type of long-term care service in their lifetime.

Unfortunately, long-term care coverage is often hindsight, only thinking about it once it is needed. Planning for it now can help you access better quality care quickly when you need it and help you and your family avoid costly claims.

How do I get long-term care insurance?

First, talk with a CERTIFIED FINANCIAL PLANNER™ about whether long-term care insurance makes sense for you. Coverage can be complex and expensive. A good Financial Advisor can help guide you to a plan that is right for you.

Most people buy their long-term care insurance through a financial advisor, however, some states offer State Partnership Programs and more employers are offering long-term care as a voluntary benefit.

It is important to start shopping before you would need coverage. While you can’t predict the future, if you wait until you are well into retirement and already having medical issues, you may be turned down or the premiums may be too high to make it a feasible option.

3. Review your Social Security Benefits

If you haven’t yet started to collect Social Security, your 65th birthday is a great time to review your Social Security strategy to help you maximize your benefits.

When can I take Social Security?

The Social Security Administration (SSA) considers the full retirement age is 66 if you were born from 1943 to 1954. The full retirement age increases gradually if you were born from 1955 to 1960 until it reaches 67. For anyone born in 1960 or later, full retirement benefits are payable at age 67.

In deciding when to start receiving Social Security retirement benefits, you need to consider your personal situation.

How can I maximize my Social Security Benefit?

Turning 65 might raise questions about how to maximize your Social Security befits in retirement. Rightfully so. Receiving benefits early can reduce your payments, however, the flip side is also true. If you’re still working or have savings that will allow you to wait a while on receiving benefits, your eventual payments will be higher. Your benefits can stand to grow 8% a year if you delay until age 70. Plus, cost of living adjustments (COLA) will also be included in that increase.

In addition to delaying receiving your benefits, it is important to make sure all your years of work have been counted. SSA calculates your benefits based on the 35 years in which you earn the most. If you haven’t clocked in 35 years, or the SSA doesn’t have those years recorded, it could hurt you.

Be sure to create a “My Social Security” account and check to make sure your work history is accurately depicted. It is wise to download and check your social security statement annually and update personal information as needed.

Another potential boost in your benefit can come from claiming spousal payments. If you were married for at least 10 years, you can claim Social Security benefits based on an ex-spouse’s work record.

Everyone’s financial situation is different, but it can be helpful to have a plan for how you’re going to approach Social Security before you turn 65.

4. Review Retirement Accounts

Even if you are not planning to retire soon, now (and every quarter for that matter) is a good time to check in on your retirement accounts. Is your portfolio allocated in a way that lines up with your target retirement date? When is the last time you met with your financial advisor? Do you need to catch up a little? Do you have a plan for your Required Minimum Distributions?

Meeting with a CERTIFIED FINANCIAL PLANNER™ can help you evaluate your risk tolerance in comparison to your retirement goals, make sure your investments are aligned to help you retire when you want, and make a plan for you to maintain the lifestyle you want in retirement.

A financial advisor can also help with planning for 401(k) catch-up contributions, RMDs, early withdrawals, or completing a Backdoor Roth.

A big hurdle as retirement approaches is often all the homework you have to do. Penalties, enrollments, coverage gaps, deadlines, etc. A great financial advisor can help guide you through this process.

If you are wondering how to find a great financial advisor, we have put a simple guide here. Or, we would love for you to schedule an appointment now to meet with one of our CERTIFIED FINANCIAL PLANNERs™.

5. Update Estate Planning Documents

The next item on the retirement checklist of important things to do when Turning 65 is to get your estate planning documents and legal ducks in a row. If you do not yet have an estate plan, will, medical directive, or financial power of attorney, it is time to get those in order. It is not too late! If you do have them, take some time to update them.

Have you had recent changes in personal circumstances? Do you need to update beneficiaries? Reviewing your plan at regular intervals, in addition to major life events, will help ensure that your assets and legacy are passed on in accordance with your wishes and that your beneficiaries receive their benefits as smoothly as possible.

Further, it is also a good idea to take inventory and organize all your financial documents. Keep a list of all your accounts (banking and investment), insurance, and estate documents as well as key contact information in a safe place. Make note of any safety deposit boxes you have. Keeping all this info organized and in one place will be a big help to your loved ones during a difficult time.

You’ll feel great knowing that you and your family are prepared

6. Get Tax Breaks

Finally, don’t let Medicare be the only gift to you when you turn 65. Starting in the year you turn 65, you qualify for a larger standard deduction when you file your federal income tax return. You may also qualify for extra state or local tax breaks at age 65.

Many states also offer senior property tax exemptions as well. For example, in Colorado for those who qualify, 50 percent of the first $200,000 of the actual value of the applicant’s primary residence is exempted. Check with your local tax assessor to see what property tax breaks may be available to you.

Turning 65 Birthday Advice

Relax and enjoy it. As much as turning 65 is a time to plan for retirement, it is also a time to celebrate.

If you plan to indulge in a much-deserved tropical getaway or a quick trip to visit your grandchildren, you may be able to take advantage of new travel discounts. Delta, American, and United Airlines all offer senior discounts on selected flights. Additionally, many hotels, car rental companies, and cruise lines all also offer senior discounts. So treat yourself!

Have more questions about turning 65 and retirement? We’d love to talk. You can reach us directly at 719-394-3900 or you can schedule a call here!

We use cookies to improve and customize your browsing experience and analyze visitor behavior. By continuing to use this site, you consent to our use of cookies. ACCEPT

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are as essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Thank You For Your Subscription

You’re in! Thanks for subscribing to our monthly newsletter. We will be sending you market updates, financial insights and inspiring travel ideas soon but in the meantime check out our blog, join us on Instagram or pop over to Pinterest.

Your Appointment Request has been Received

Thank you for reaching out! We are excited to learn more about you. Someone from our team will be in touch shortly.

Sign up now

Join us around the fire for monthly market updates, financial insights and inspiring travel ideas.

Client Login

Client Login