Client Login

Client Login

The Most Overrated Retirement Assets

When most people think about building wealth in retirement, they focus on buying more assets. More real estate, more investments, more financial products. More “opportunities.” But wealthy retirees often think very differently. Instead of chasing every investment idea that gets pitched to them, they focus heavily on simplicity, cash flow, flexibility, and avoiding unnecessary financial drag.

That distinction matters.

Some retirement assets look impressive on paper but quietly create stress, reduce liquidity, increase fees, or slowly eat away at retirement income over time. Others are sold aggressively because they generate commissions for someone else, not because they are necessarily the best fit for your situation.

We regularly meet retirees who own assets they barely understand, properties that lose money every month, or financial products that sounded great in the sales presentation but became frustrating later. The goal is not to say every one of these retirement assets is automatically bad. In some cases, they can absolutely make sense. The key is understanding whether the asset truly supports your retirement lifestyle and long-term financial goals.

Here are eight retirement assets wealthy retirees often avoid, or at the very least approach with much more caution.

Keep reading, or if you prefer to listen or watch… check out the Podcast or full YouTube video.

1. Investment Real Estate That Does Not Cash Flow

Real estate can absolutely be a fantastic investment. Many wealthy individuals have built substantial wealth through real estate ownership.

But there is a major difference between owning productive real estate and owning a property that consistently drains your cash flow.

One of the most common retirement asset mistakes people make is buying investment properties that lose money every month while convincing themselves the appreciation will eventually make it worthwhile. Often the justification becomes:

“It’ll be paid off someday.”

The problem is that retirement is about cash flow now, not just theoretical future equity decades later.

If a property requires constant subsidizing, expensive maintenance, ongoing repairs, rising insurance premiums, and unpredictable tenant issues, it may not actually be serving your retirement lifestyle the way you think it is.

That does not mean every property must generate massive profits immediately. Some investors intentionally pursue appreciation-focused strategies. But wealthy retirees usually understand exactly why they own a property, what role it serves, and whether it is helping or hurting their financial picture.

The key question is simple:

Is this retirement asset improving your life and strengthening your finances, or is it becoming a burden?

2. Complex Financial Products You Do Not Understand

One thing wealthy retirees often avoid is unnecessary complexity.

Many financial products sound incredibly appealing because they promise downside protection, enhanced income, or sophisticated strategies unavailable to average investors. Structured notes and highly engineered financial products are often marketed this way.

The issue is not necessarily that these products are always bad. Some can absolutely serve a purpose in certain situations.

The problem is when people buy retirement assets they do not truly understand.

If you cannot clearly explain:

- How the investment works

- What risks exist

- When you can access your money

- How returns are generated

- What the fees are

then you probably should not own it.

Wealthy retirees who sleep well at night often prioritize clarity over complexity. They know where their money is, what it is doing, and why they own it. That level of simplicity becomes incredibly valuable in retirement.

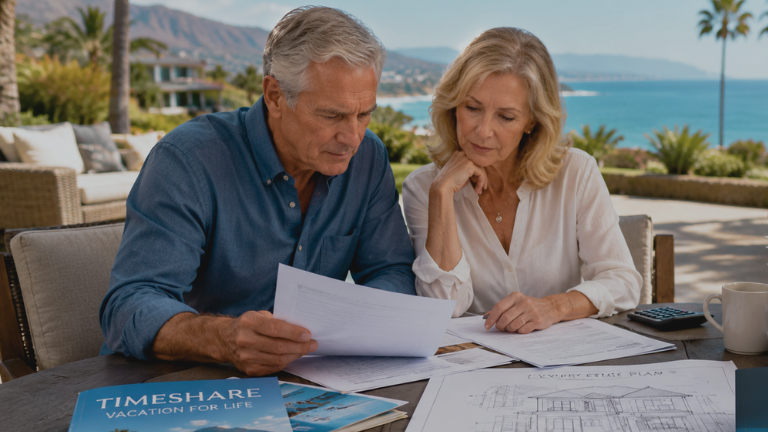

3. Timeshares

Timeshares are one of the most heavily sold retirement assets on the market.

The sales presentations are designed to feel emotional and exciting. Beautiful resorts, family memories, beachfront views, luxury vacations, and the promise of saving money long-term can make timeshares sound extremely appealing in the moment.

But the reality often looks very different later.

Many retirees eventually realize they committed themselves to:

- Long-term contracts

- Ongoing maintenance fees

- Limited flexibility

- Rising costs

- Difficult resale markets

Life changes over time. Health changes. Travel preferences change. Family dynamics change.

A vacation property that seemed perfect ten years ago may no longer fit your lifestyle today.

Wealthy retirees often value flexibility more than people realize. Instead of locking themselves into long-term vacation commitments, many prefer the freedom to travel wherever they want, when they want, without ongoing contractual obligations.

The issue is not necessarily the vacation itself. The issue is becoming financially trapped by an asset that no longer serves your lifestyle.

4. Whole Life Insurance as an Investment

Insurance is incredibly important.

But insurance and investing are not always the same thing.

One of the more controversial retirement assets is whole life insurance used primarily as an investment vehicle. These policies are often marketed as:

- Forced savings

- Tax advantages

- Borrowing opportunities

- Stable growth

- Wealth-building tools

And while there are situations where whole life insurance absolutely makes sense, many retirees end up purchasing expensive policies that may not align with their actual needs.

One major issue is cost.

Whole life insurance policies can involve:

- High premiums

- Significant commissions

- Slow early growth

- Complex structures

- Lower long-term returns compared to other investments

That does not automatically make them bad. But wealthy retirees typically understand exactly why they are purchasing a policy before committing to one.

If the primary need is protecting a spouse or family financially, there may be simpler and more efficient ways to accomplish that goal.

This is why many retirees should approach whole life insurance carefully rather than assuming it is automatically a strong investment.

5. High-Fee Annuities

Annuities are another retirement asset that can create strong opinions.

The truth is, annuities are not inherently bad. In fact, some retirees benefit tremendously from them.

At their core, annuities function somewhat like personal pensions by providing guaranteed income streams.

That can be extremely valuable in retirement.

However, many retirees buy annuities without fully understanding:

- The fees

- Liquidity restrictions

- Tax implications

- Surrender periods

- Income limitations

Some annuities contain fees that quietly reduce returns year after year. Others lock up money for extended periods, making access difficult without penalties. This becomes especially problematic when retirees need flexibility later.

Wealthy retirees often avoid retirement assets that unnecessarily trap capital or create confusion. If they use annuities, it is usually because the product fits a very specific need within an overall retirement strategy.

Not because it was aggressively sold as a one-size-fits-all solution.

6. Vacation Homes That Become Financial Burdens

Vacation homes sound amazing in theory.

And for some wealthy retirees, they absolutely can be.

But there is an important difference between enjoying a second home and becoming financially overextended because of one.

Many retirees underestimate the true cost of owning multiple properties. Beyond the mortgage itself, there are:

- Taxes

- Insurance

- Maintenance

- Utilities

- Repairs

- Furnishing costs

- HOA fees

- Travel expenses

In some cases, retirees discover they spend more time maintaining the property than actually enjoying it.

Instead of feeling like a relaxing escape, the property slowly becomes another responsibility.

Wealthy retirees tend to evaluate retirement assets based on lifestyle value, not just emotional appeal. If a second home genuinely improves quality of life and fits comfortably within the financial plan, that is one thing.

But if it is creating stress, adding too many expenses, reducing flexibility, or draining cash flow, it may no longer be serving its intended purpose.

Sometimes renting luxury vacations when desired creates far more freedom than owning another home full-time.

7. High-Fee Actively Managed Mutual Funds

Many retirees assume actively managed mutual funds must be superior because professional managers are selecting investments on their behalf.

But statistics consistently show that many actively managed funds underperform their benchmarks over long periods of time, especially after fees.

This becomes one of the biggest hidden problems with certain retirement assets.

Fees matter enormously over time.

Even small percentage differences can compound into substantial reductions in long-term wealth over decades.

Wealthy retirees often focus heavily on:

- Low costs

- Tax efficiency

- Diversification

- Simplicity

- Long-term consistency

That is one reason index investing has become increasingly popular.

The issue is not that every actively managed fund is bad. Some managers absolutely outperform. The challenge is identifying them consistently in advance.

Many retirees end up paying high fees for performance that ultimately fails to justify the added cost.

8. Oversized Homes

A home is not automatically a bad retirement asset.

But oversized homes can quietly become major financial drains in retirement.

Many retirees remain in houses far larger than what they realistically use because of emotional attachment or habit. Meanwhile, the ongoing costs continue rising:

- Property taxes

- Insurance

- Utilities

- Repairs

- Landscaping

- Cleaning

- Maintenance

A large home can also create physical stress as people age.

Wealthy retirees often prioritize functionality and lifestyle over simply owning the biggest house possible. They understand that reducing unnecessary overhead can significantly improve retirement flexibility and reduce financial pressure.

This does not mean everyone should downsize immediately. But retirees should honestly evaluate whether their current home still serves their life today or whether it is simply consuming resources unnecessarily.

Sometimes simplifying housing creates one of the biggest quality-of-life improvements in retirement.

The Common Theme Behind These Retirement Assets

Every retirement asset on this list shares something in common.

They often:

- Look impressive initially

- Are heavily sold

- Sound financially sophisticated

- Create hidden costs

- Reduce flexibility

- Add complexity

- Slowly transfer value away from the owner

Wealthy retirees who feel financially secure often approach retirement differently.

They tend to value:

- Cash flow

- Simplicity

- Liquidity

- Flexibility

- Low fees

- Clear understanding

- Lifestyle alignment

They know exactly what their money is doing and why they own each asset.

That level of clarity becomes incredibly important in retirement because complexity often creates stress, confusion, and hidden financial inefficiencies.

Simplicity Often Wins in Retirement

One of the biggest misconceptions about wealth is that wealthy retirees own the most complicated portfolios or sophisticated financial products.

In reality, many financially successful retirees keep things surprisingly simple.

They focus on:

- Strong cash flow

- Tax efficiency

- Low costs

- Diversification

- Flexibility

- Assets they fully understand

Retirement should ideally create freedom, not additional stress.

The goal is not accumulating impressive-sounding retirement assets. The goal is building a financial life that supports your lifestyle, protects your long-term security, and gives you confidence moving forward.

Final Thoughts

Not every retirement asset is automatically good or bad.

The real question is whether the asset aligns with your goals, cash flow needs, risk tolerance, and retirement lifestyle.

Many retirement products are marketed aggressively because they generate commissions, fees, or long-term contracts. That does not mean they are wrong for everyone. But it does mean retirees should approach them carefully and fully understand what they are buying before committing.

At Bonfire Financial, we believe retirement planning works best when people clearly understand how every piece of their financial picture fits together. If you want help evaluating your retirement assets and building a coordinated retirement strategy, learn more about The Bonfire Method and schedule a conversation with our team.