Client Login

Client Login

If you’re looking for a low-risk, predictable way to grow your money, investing in CDs (Certificates of Deposit) might be worth a second look. While they might not be the flashiest option in your portfolio, CDs offer stability, security, and in today’s market, surprisingly decent returns. Let’s break down what CDs are, how they work, and why they might deserve a spot in your financial plan.

Listen Now: iTunes | Spotify | iHeartRadio | Amazon Music

What Is a CD (Certificate of Deposit)?

A Certificate of Deposit is a financial product offered by banks and credit unions. It allows you to deposit money for a fixed period, typically ranging from three months to five years, in exchange for a guaranteed interest rate. In return, you agree not to withdraw your funds during that term without paying a penalty.

The trade-off?

A higher interest rate than you’d typically earn from a traditional savings account. Plus, your investment is protected by FDIC (Federal Deposit Insurance Corporation) insurance, up to $250,000 per depositor, per bank, which provides peace of mind and a sense of financial security. CDs are often seen as a great way to safeguard cash that you want to grow without exposure to market volatility. They’re straightforward, easy to understand, and come in a variety of terms that fit most savings goals.

Why CDs Are Gaining Popularity Again

In recent years, low interest rates made CDs less appealing. But as interest rates have risen, so have CD yields. In some cases, one year CDs have offered rates exceeding 5%, which is competitive with many bonds but with less risk and complexity. In a time when inflation and market volatility are top of mind for investors, CDs have become a compelling option. With guaranteed returns and federal insurance backing, they offer peace of mind in uncertain times.

Another reason for renewed interest is that CDs can serve as a temporary parking place for cash you may not need immediately. For example, if you plan to buy a home in the next year or want to set aside funds for a child’s tuition, a CD allows that money to earn more than a savings account while remaining protected.

Understanding CD Laddering: A Smart Strategy

One challenge with investing in CDs is that your money is locked up for a set time. That can create issues if you need liquidity. Enter: CD laddering.

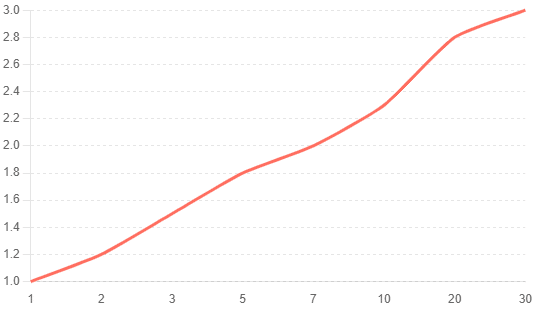

CD laddering is a strategy that involves opening multiple CDs with different maturity dates. For example:

- 3 month CD

- 6 month CD

- 9 month CD

- 12 month CD

As each CD matures, you reinvest the money into a new 12 month CD. Over time, you’ll have a CD maturing every quarter, providing access to your funds without sacrificing returns. This strategy gives you the best of both worlds: higher returns from longer term CDs and consistent access to cash.

Why laddering works:

- Provides ongoing liquidity

- Takes advantage of rising rates

- Reduces the impact of rate fluctuations

- Helps maintain a balanced, conservative cash management approach

Laddering is especially effective when you’re managing cash for short to medium term goals but still want to earn something meaningful on your money.

The Safety Net: FDIC Insurance

One of the biggest advantages of investing in CDs is the built in safety net: FDIC insurance. If your bank fails, the federal government covers your deposit (up to $250,000 per depositor, per bank). This makes CDs one of the safest investment vehicles available.

Want to invest more than $250,000? You can still stay insured by spreading your CDs across multiple banks. For high net worth individuals, brokered CDs, offered by firms like Schwab, Fidelity, or Merrill Lynch, allow you to manage large CD portfolios and stay within insurance limits.

Brokered CDs vs. Traditional Bank CDs

Traditional CDs are offered by your local bank or credit union. Brokered CDs, on the other hand, are sold through investment firms and allow you to:

- Access CDs from multiple banks

- Get competitive rates

- Stay within FDIC insurance limits

- Integrate CD investing into a broader portfolio with a financial advisor

However, brokered CDs may have less flexibility for early withdrawals. If you need to cash out early, you’ll likely have to sell it on the secondary market, and that could result in a loss if rates have risen since your purchase. That’s why brokered CDs are better suited for those who are confident they won’t need to touch the funds before maturity.

What Happens if You Need to Cash Out Early?

CDs aren’t known for their liquidity. If you break a CD before it matures, you may face penalties:

- Bank CDs: Early withdrawal fees, typically a portion of the interest earned.

- Brokered CDs: You’ll need to sell on the open market, where prices fluctuate with interest rates.

That’s why planning your liquidity needs is critical. CD laddering can help here, but make sure you have other liquid assets available for emergencies. A good rule of thumb is to keep 3 to 6 months of living expenses in a highly liquid account, like a savings or money market account.

Comparing CDs to Other Investments

Bonds vs CDs:

- CDs are FDIC insured; most bonds are not.

- Bonds may offer higher returns but come with credit and market risk.

- Bonds fluctuate in value; CDs pay a fixed return if held to maturity.

Savings Accounts vs. CDs:

- CDs generally offer higher interest rates.

- Savings accounts offer better liquidity and flexibility.

- CDs require committing to a time period; savings accounts do not.

Money Market Accounts vs CDs:

- CDs can have better fixed rates.

- Money markets offer variable rates and check-writing privileges.

- Both may be FDIC insured but have different liquidity profiles.

When Do CDs Make Sense?

CDs are ideal if:

- You’re saving for a specific short to mid term goal

- You’re risk averse and want principal protection

- You don’t need immediate access to the funds

- You’re looking for a place to earn interest on cash you’ve already set aside

Common use cases:

- Emergency reserves (when laddered)

- Saving for a home, car, or large future purchase

- Parking cash during market volatility or downturns

- Stashing business reserves for tax or payroll obligations

Risks and Downsides of Investing in CDs

While CDs are low risk, they’re not risk free:

- Inflation Risk: If inflation rises significantly, your CD’s return may lose purchasing power.

- Liquidity Risk: Your money is tied up unless you’re willing to pay a penalty or take a loss.

- Opportunity Cost: If interest rates rise after you lock in a CD, you miss out on the higher return.

The key is balance. CDs shouldn’t be your only investment, but they can serve an important role alongside more aggressive or growth-focused strategies.

Maximizing CD Returns

To get the most from CD investing:

- Compare rates across institutions and platforms

- Use CD ladders to maintain flexibility and manage cash flow

- Look into brokered CDs if you’re managing large balances

- Reinvest matured CDs at new, higher rates if available

- Avoid tying up all your liquid cash, keep a buffer in savings

Online banks and credit unions often offer higher CD rates than brick and mortar institutions. Keep an eye on rate changes, especially in a rising rate environment.

Final Thoughts: Are CDs Right for You?

Investing in CDs isn’t going to make you rich overnight, but they can be a smart, low-risk part of your portfolio, especially when rates are attractive. Whether you’re building a ladder, protecting a cash reserve, or just looking for a better alternative to your savings account, CDs offer a blend of security and predictability that’s hard to beat.

As always, your overall financial goals, timeline, and risk tolerance should guide your decision. CDs are one tool in the toolbox, but when used strategically, they can help you sleep better at night, knowing your money is working for you.

Next Steps

If you want help deciding if CDs fit your financial plan, let’s talk. Schedule a consultation call today!