Client Login

Client Login

United Airlines Employee Benefits: Retirement Health Account

Working as a United Airline Employee has more benefits than just a 401(k) plan or free flights. United provides a Retirement Health Account that gives you another resource to fund medical expenses in retirement. When doing financial plans for our clients, many of which are pilots, one important issue that often comes up is how to fund health care. The United RHA is a great tool for that.

What is an RHA?

The United Retirement Health Account is a health expense reimbursement account like a Health Saving Account (HSA) but one you use in retirement. United Airlines ALPA Retirement Health Account (RHA) allows retired United and legacy Continental pilots to reimburse themselves tax-free for qualified health expenses for them, their spouses, and dependents in retirement. For that reason, it truly is one of the great United Employee benefits.

Eligible expenses include:

- Doctor visits

- Co-pays

- Dental premiums

- Insurance premiums

- Medicare

- Long Term Care insurance premiums

The RHA is a fringe benefit provided by United and is a unique savings account that most companies do not have. United basically got the blessing of the IRS through a private letter ruling to have this plan. Because it is more of a one-off plan the rules are more opaque and restrictive.

How does the RHA work?

Unlike other United Airlines employee benefits, the RHA is funded by United only. No employee money is ever contributed to the account. Every working hour, United contributes $1.00 to your account. More importantly, when your 401(k) limit is reached, all employer contributions will continue, but spill into the RHA.

United contributes a % of your salary into your 401(k), and once the 401(k) limit is reached further contributions will spill into the RHA. Forfeited vacation can be contributed to either the PRAP or RHA at the employees’ discretion. Schedule a call with us to discuss the current limits and how to maximize this.

What can I use the RHA for?

The RHA is meant for medical expense reimbursement in retirement or separation of service only. The account itself is held in a pooled account with other employees and pilots at United, and cannot be moved into an individual account. As such, the benefit of the RHA is to allow you and your spouse and dependents to reimburse any health expenses and premiums tax-free.

According to a study done by Fidelity, the average 65-year old couple retiring can expect to spend $285,000 in healthcare and medical expenses. Medical expenses increase at nearly twice the rate of inflation, and will likely continue to grow in the future. The RHA allows retired employees and pilots to maximize their retirement benefits by providing a tax-free vehicle to pay for medical expenses, without having to access taxable or tax-deferred accounts like your 401(k).

An Example

Take for example, Sarah. Sarah is a retired pilot and can use her 401(k) to pay for regular retirement expenses. The issue that she runs into is that distributing from her 401(k) will recognize that income. If she is currently in the 22% tax bracket and takes out $50,000 per year to pay for expenses, she will need to pay $11,000 in tax for that year. Sarah needs surgery and will need to pay $10,000 out of pocket. She will pay that money from her checking account, and reimburse herself from the RHA for $10,000. Because she used the RHA for a qualified health expense, she will not have to pay any taxes. If Sarah made the mistake of using her 401(k) for the expense, she would need to pay an extra $2,200 to the government!

The RHA can be used to pay for Medicare premiums, co-pays, insurance premiums, dental insurance premiums and expenses, and even long-term care insurance premiums. The RHA can grow rather quickly and it can be very useful for your family. For example, if you have a balance of $0 in your RHA, and United contributes $5,000 each year for 20 years, and you expect an annual return of 6%, your ending RHA value will be $183,928 of tax-free dollars at 65! If you have contributed $10,000 per year, you would have $367,856!

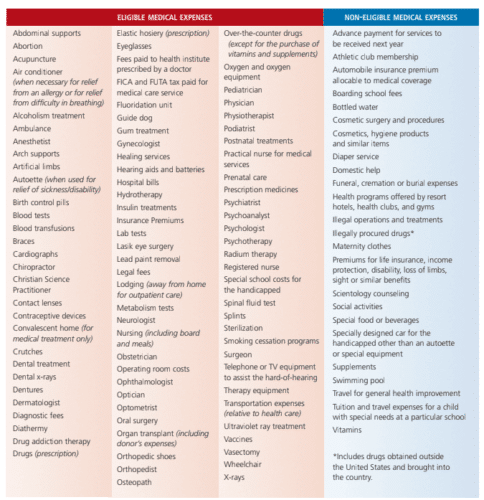

Eligible Expenses

All of the following in red are covered by the RHA. The blue are non-eligible medical expenses that must be paid out-of-pocket.

(Image: Further/SelectAccount Family of Products)

When can I access the money in my RHA?

There are a few times in which you will be able to access your RHA. The most straightforward one is in retirement. Also, if you are laid off or fired you will be able to access it. Additionally, if you are furloughed, you can use the RHA to pay for COBRA premiums until you get back to work. Just another one of the United Employee Benefits.

How do I maximize my RHA?

If you are nearing retirement, you may be seeing that you have a very large 401(k), which can also mean a very large tax problem when you go to withdraw from it in retirement, especially with Required Minimum Distributions (RMD) as of 2025 beginning at 73 years old with the new SECURE retirement act. To maximize RHA funding, you can contribute more to your 401(k).

Say if you make $280,000 in 2020, United will contribute $44,800. Because there is only $37,500 left for United to fund the 401(k), the rest, $7,300, will spill into the RHA. Therefore, if you wish to save more in your RHA, you can maximize your contribution early in the year to fund the 401(k) using your employee contribution.

Further, you can also elect to move all forfeited vacation days into the RHA. You can maximize or minimize what is in your RHA by either over- or under-funding your PRAP using your employee contribution or forfeited vacation. The United Retirement & Insurance Committee has an RHA spill calculator available to you, to estimate your projected RHA funding.

Here is an example of two pilots, they both make $280,000. Both pilots are 47 years old. Tom (Pilot A) maxes his 401(k) contribution up to $19,500. Bill (Pilot B) contributes $10,000 to his 401(k). Remember, the total amount allowed in the 401(k) per year is $57,000. Any amount over will spill into the RHA:

| Salary | United’s 16% Contribution | Pilot’s Personal Contribution | Total Contribution (limit of $57,000) | Spill into RHA (above $57,000) | |

| Tom (A) | $280,000 | $44,800 | $19,500 | $64,300 | $7,300 |

| Bill (B) | $280,000 | $44,800 | $10,000 | $54,800 | $0 |

>> Click here for the current year’s contribution limits. <<

How do I limit contributions to my RHA?

Because United funds your RHA based on your salary, there is no way to avoid contributing to the RHA if United has maximized your 401(k) contribution. All employer contributions will go to the RHA after that. By underweighting what you contribute into the 401(k), you can limit the amount of spill into the RHA. Regardless, you are not losing money when United contributes to the plan. It is essentially a free benefit to you.

What happens to my RHA if I die?

The RHA can be used by you, your spouse, and qualified dependents. If you are 65, and your children now support themselves, they are not considered to be your dependent. When you die, your spouse will be able to use and access the RHA. Once your spouse dies, and you have no dependents, any remaining amount in the RHA will be reverted back into the pooled investment account at the record keeper. The RHA is not able to be inherited like other accounts. Therefore, it is important to take advantage of your RHA when you are able to use it so you don’t leave any money on the table.

The RHA and Tricare for Life

Many pilots are retired military and will use Tricare to supplement part of their medical coverage. For example, a family on Tricare for Life in retirement will still be using Medicare Part A & B, and Tricare is used in conjunction to pay for coverage outside of hospital stays (A) and doctor’s visits (B). Similarly, Tricare is used for other coverage such as prescription drugs, and the remaining premiums from Medicare Part B. Tricare and Medicare Part A & B cover most health-related expenses, but the RHA can be used tax-free to cover other parts such as dental insurance premiums, long term care insurance premiums, vision plans, therapy, and other eligible medical expenses outside of Medicare and Tricare coverage.

RHA to fund long term care insurance premiums

According to Genworth Insurance, $51,480 in 2019 was the national annual median cost of In-Home Care. Long-term care can quickly drain older Americans’ retirement and savings. According to AARP, 52% of people turning 65 in 2017 will need long-term care at some point. The estimated cost for end-of-life care in 2016 ranged from $215,820 and $341,651 according to Alzheimer’s Association. Ultimately, the last thing you want is to drain your worth in your final years and not be able to leave anything to your estate, children, heirs, and charities.

Long-term care insurance is one way to pay for long-term care and nursing care. LTC insurance can be costly. Luckily, you can pay for LTC insurance premiums tax-free with the RHA. Therefore, you can have LTC insurance and leverage your RHA’s tax-free characteristics.

The Retirement Health Account might just be one of the best United employee benefits out there. It’s employer-funded, more money without more taxes, and extra money for health care expenses during retirement.

Questions?

We are here to help. Bonfire Financial acts as a fiduciary financial advisor for our clients. We have a staff of Certified Financial Planners™ that specialize in helping United Airline Employees and Pilots with their retirement and benefits. Schedule a free consultation with us today. We’d love to talk to you.