Client Login

Client Login

Nothing says “I love you” like chocolates, flowers, and… updating your beneficiaries? That’s right! While it may not sound as romantic as a candlelit dinner, making sure your assets go to the right people is one of the most thoughtful things you can do for your loved ones.

Life happens—marriages, divorces, new babies, and unexpected events can change everything. Yet, many people forget to review and update their beneficiary designations, potentially leaving their hard-earned money to an ex-spouse, estranged relative, or even the government (yikes!).

Today we’ll break down why updating your beneficiaries is crucial, common mistakes to avoid, and how to make sure your financial love story has the perfect ending.

Listen anywhere you stream Podcasts

iTunes | Spotify | iHeartRadio | Amazon Music

__

What Is a Beneficiary? And Why Does It Matter?

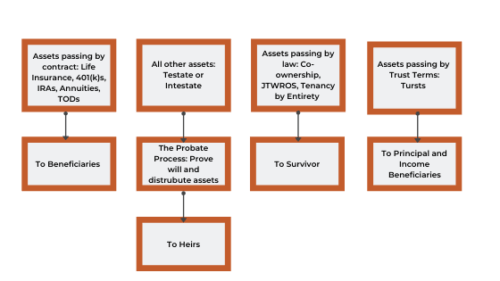

A beneficiary is the person (or people) who will receive your assets—such as life insurance, retirement accounts, or investment accounts—when you pass away. Naming a beneficiary ensures your money goes exactly where you want it, without going through probate, the long and costly legal process of settling your estate.

Many financial accounts allow you to name both:

- Primary beneficiaries – The first person(s) in line to receive the assets

- Contingent beneficiaries – The backup(s), in case the primary beneficiary is no longer living

Where Do You Need to Name Beneficiaries?

You can and should assign beneficiaries to:

- 401(k) and IRA accounts

- Life insurance policies

- Annuities and pensions

- Brokerage and investment accounts (via a Transfer on Death designation)

- Bank accounts (via Payable on Death designation)

- Trusts and estate plans

If you don’t name a beneficiary—or if your beneficiary is outdated—your assets may default to your estate and be subject to probate, causing delays, unnecessary taxes, and legal battles.

Common Beneficiary Mistakes to Avoid

1. Forgetting to Update After Life Changes

Major life events often impact financial plans. You might:

- Get married but forget to update your 401(k), still listing your parents as beneficiaries.

- Have kids but never add them as contingent beneficiaries.

- Get divorced but still have your ex-spouse listed as your life insurance beneficiary.

If you don’t update your beneficiary designations, your assets may end up in the wrong hands.

2. Leaving It Blank

If you never designate a beneficiary, your assets will go to your estate by default. This means probate court decides who gets what, which can lead to delays, legal fees, and unintended consequences.

3. Not Naming Contingent Beneficiaries

A primary beneficiary is important, but what if they pass away before you do? Without a contingent beneficiary, your assets could be tied up in probate.

4. Unequal Distribution

If you have multiple beneficiaries, double-check the percentages assigned. Mistakenly leaving one person out or assigning uneven percentages could cause family tension.

5. Naming Minor Children Directly

Children under 18 cannot legally inherit assets directly. If you name them as beneficiaries, the court will appoint a guardian to manage the funds. Set up a trust to make sure everything is how you want it.

6. Assuming a Will Covers It

Even if your will states who should inherit your assets, beneficiary designations on financial accounts override a will. If your will and your beneficiary list don’t match, the beneficiary designation takes precedence.

7. Naming a Trust Incorrectly

Trusts can be a powerful estate planning tool, but they must be properly structured and funded. If your accounts are not titled correctly or beneficiaries aren’t aligned with the trust, the trust won’t control those assets as intended.

8. Forgetting to Update Employer Retirement Accounts

Your old 401(k) from a previous employer might still list your parents, an ex, or someone else you no longer intend to inherit your funds. Make sure to update all employer-sponsored accounts whenever you switch jobs.

How to Review and Update Your Beneficiaries

Updating beneficiaries is easier than you think. Here’s how to do it:

Step 1: Make a List of Your Accounts

Look at all your financial accounts that have beneficiaries, including:

- Retirement accounts (401k, IRA, Roth IRA, pension plans)

- Life insurance policies

- Bank and brokerage accounts

- Annuities and investment accounts

- Trusts and estate documents

Step 2: Verify Your Current Beneficiaries

Log into your accounts or call your financial institution to check:

- Who is currently listed as your primary and contingent beneficiaries?

- Are the names, relationships, and percentages correct?

Step 3: Make Necessary Updates

To update your beneficiaries, you’ll typically:

- Log into your financial institution’s website or request a beneficiary form.

- Choose your primary and contingent beneficiaries.

- Assign percentages to each beneficiary.

- Review the changes and submit the form.

It’s a good practice to update beneficiaries once a year or after major life changes, such as marriage, divorce, or the birth of a child.

Special Situations: Who Should You Name as a Beneficiary?

1. If You are Married:

- Your spouse is typically the default primary beneficiary.

- Name a contingent beneficiary (children, trust, or charity) in case your spouse predeceases you.

2. If You Have Kids:

- Avoid naming minor children directly. Instead, use a trust or custodial account to manage the funds.

3. If You’re Divorced:

- Remove your ex from your beneficiary list if they’re still listed.

- Consider naming children, a new spouse, or a trust instead.

4. If You’re Single With No Kids:

- Consider naming siblings, parents, nieces, nephews, or a charity.

5. If You Have a Trust:

- Make sure your trust is properly funded and your beneficiaries align with it.

Final Thoughts: The Greatest Love Letter You’ll Ever Write

Estate planning and beneficiary updates might not be the most romantic topic, but they are one of the greatest gifts you can give to your loved ones. By keeping your designations up to date, you ensure that your hard-earned money goes exactly where you want it—without confusion, legal headaches, or financial heartbreak.

This year, take a few minutes to review your beneficiaries. It’s a small step that can make a huge difference for those you love.

If you need help reviewing your overall plan? We’d love to help. Schedule a call with us today!