Client Login

Client Login

Common Investing Mistakes (And How to Fix Them)

Most people think investing is about picking the right stock or timing the market, but that’s not what actually builds lasting wealth.

In reality, some of the biggest investing mistakes aren’t made by beginners. They’re made by high earners who are doing a lot of things right, but still feel like something is off.

They’re saving, they’re investing. They have a 401(k). On paper, everything looks solid.

And yet, there’s still uncertainty. Still hesitation. Still the question: am I actually doing this the right way?

After years of working with clients on financial planning, retirement strategy, and long-term investing, the patterns become clear. The issue usually isn’t effort. It’s structure. It’s mindset. And it’s a handful of common investing mistakes that quietly compound over time.

If you want to build real wealth and actually feel confident in your financial life, these are the mistakes worth paying attention to.

Keep reading, or if you prefer to listen or watch…check out the Podcast or full YouTube video.

Mistake #1: Thinking Investing Is About Picking Winners

One of the most common investing mistakes is believing that success comes from finding the next big stock.

High earners are often smart, analytical, and used to solving problems. So naturally, they approach investing the same way. They try to outthink it. They look for the edge. The opportunity others are missing.

But investing doesn’t reward that behavior consistently.

Real wealth is not built on a few big wins. It’s built on consistency over time. It’s built on a system that works regardless of headlines, trends, or market noise.

The sooner you shift from trying to pick winners to focusing on a repeatable strategy, the sooner things start to click.

Mistake #2: Relying Too Heavily on a 401(k)

A 401(k) is a great tool, but it’s not a complete strategy.

This is one of the most common investing mistakes high earners make. They do exactly what they were told, contribute consistently, and they take the match. And over time, they build a meaningful balance.

But then they realize most of their wealth is locked away.

That creates a lack of flexibility. If you want to retire early, invest in something outside the market, or simply have access to capital before traditional retirement age, your options become limited.

The solution isn’t to avoid a 401(k). It’s to avoid relying on it exclusively. Building wealth the right way means having multiple buckets, each serving a different purpose.

Mistake #3: Letting Too Much Cash Sit Idle

Another common investing mistake is holding excessive cash.

This often comes from a good place. It feels safe. It feels responsible. Especially for high earners who have worked hard to build what they have.

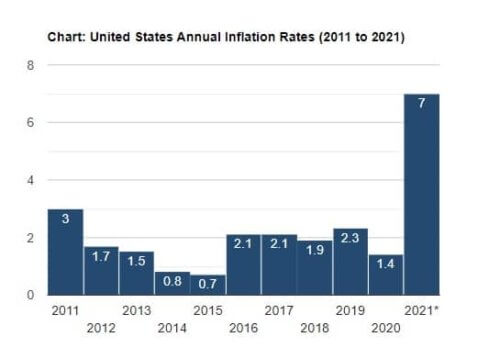

But over time, idle cash quietly loses value mostly due to inflation. It doesn’t grow. It doesn’t compound. And it doesn’t contribute to long-term wealth in any meaningful way.

The goal isn’t to eliminate cash completely. It’s to be intentional about how much you keep liquid and how much you put to work.

Mistake #4: Waiting Until Everything Feels “Perfect”

A lot of high earners delay making decisions because they want to get it right.

They want the right strategy, the right timing, the right plan.

The problem is that waiting is its own decision, and it usually costs more than getting started imperfectly.

Compounding only works if you give it time. The longer you wait, the more you give up.

You don’t need a perfect plan to start building wealth. You need a solid foundation and the willingness to move forward.

Mistake #5: Confusing Income With Financial Security

Making more money does not automatically lead to feeling secure.

This is one of the most overlooked investing mistakes. High earners often assume that as income increases, everything else will fall into place.

But without structure, higher income can actually create more complexity.

More accounts, more decisions, and more variables.

Financial confidence doesn’t come from income. It comes from clarity. It comes from knowing how everything fits together and why you’re doing what you’re doing.

Mistake #6: Ignoring the Role of Mindset

Many investing mistakes aren’t technical. They’re behavioral.

If someone grows up with a scarcity mindset, that doesn’t disappear when their income increases. It often carries forward into how they save, spend, and invest.

That can lead to hesitation, second-guessing, or an inability to enjoy what they’ve built.

On the flip side, overconfidence can lead to unnecessary risk and poor decisions.

Building wealth isn’t just about numbers. It’s about how you think about money and how that thinking shows up in your actions.

Mistake #7: Overcomplicating the Strategy

High earners are used to complexity in their professional lives, so they often assume investing needs to be complex as well.

It doesn’t.

In fact, complexity is often one of the biggest barriers to success.

The fundamentals are simple. Have a solid foundation. Invest consistently. Use the right mix of accounts. Stay disciplined over time.

It’s not flashy. But it works.

What Actually Builds Wealth Over Time

If these are the most common investing mistakes, what does the right approach look like?

It starts with a foundation.

An emergency fund that covers three to six months of expenses. No high-interest consumer debt. Stability before growth.

From there, it’s about using the tools available to you.

Taking advantage of employer matches. Building additional investment accounts that provide flexibility. Creating a structure that supports both long-term growth and short-term access.

And then, most importantly, staying consistent.

Investing month after month. Letting compounding do its job. Avoiding the temptation to constantly adjust based on what’s happening in the moment.

Why Consistency Beats Timing

Trying to time the market is one of the most common investing mistakes, even among experienced investors.

The problem is that it requires being right twice. When to get in and when to get out.

Consistency removes that pressure.

When you invest regularly over time, you smooth out the highs and lows. You participate in growth without needing to predict it.

And over the long run, that approach tends to outperform most attempts at timing.

The Difference Between Looking Wealthy and Being Wealthy

There’s a difference between looking successful and actually being financially secure.

Looking wealthy is often tied to visible things. Cars, homes, lifestyle.

Building wealth happens behind the scenes. It’s in the structure. The discipline. The decisions no one sees.

Many people who appear wealthy are financially fragile. And many people who are truly wealthy don’t feel the need to prove it.

Understanding that difference changes how you approach money.

What a Rich Life Actually Means

At some point, the definition of wealth shifts.

It moves away from accumulation and toward freedom.

The ability to make decisions without financial pressure. To spend time how you want. To create experiences with people you care about.

That’s what money is supposed to support.

Not just a number, but a life that you actually enjoy living.

Final Thoughts

Most investing mistakes don’t feel like mistakes in the moment.

They feel reasonable, they feel safe, and they feel like the right thing to do.

But over time, they add up.

The good news is that the solution isn’t complicated.

It’s about focusing on the fundamentals. Building the right structure. And staying consistent long enough for it to work.

If you can avoid the common investing mistakes high earners make and shift your approach toward clarity and simplicity, you put yourself in a completely different position.

Not just to build wealth, but to actually enjoy it.

Next Steps

Reading about investing mistakes is one thing. Fixing them in your own situation is another.

The Bonfire Method is designed to give you a clear plan across every part of your financial life, not just your investments. In 30 days, you’ll know exactly where you stand and what to do next.

If you’re ready to get out of the guesswork and into a real strategy, you can apply here.